College is an investment in your child and your family, but it can come at a hefty price. Here are some tips to save!

College and other forms of higher education have always been a vital part of planning a career. The foundation of any resume, a recent study interviewing 500 professional recruiters showed that all 500 look for candidates with a college degree [1]. Some common rebuttals to the argument for college might start with names like Zuckerberg, Jobs, Gates and Oprah Winfrey, all who dropped out school. Those four have incredible stories, but they’re the exception, not the rule.

The average college graduate with a bachelor’s degree has a lifetime earnings of $2.8 million while a person who achieved a high school diploma earns an average of $1.6 million over their career[2]. At the same time, that average increase in lifetime earnings can come at a steep price, and that price is only rising. Tuition has climbed 211% for in-state universities over the last 20 years [3], escalating panic in students and their families who are forced to shoulder the burden. Without a plan to tackle them, loans can hang over a student’s head for decades. To alleviate some of that stress, here are a few tips for saving for and funding your child’s college education:

- Assess early options

Many high schools around the United States offer Advanced Placement (AP) and dual-enrollment classes. By taking these higher-level courses while still in high school, students can be awarded college credits early, potentially at an even lower cost. AP classes are generally more difficult classes targeting more specific areas of study within a subject. They’re widely accepted and acknowledged throughout U.S. colleges, and they are free to students who elect to take the challenge. End-of-year tests for AP classes do cost $96 per exam [4] in the U.S., but colleges may award credits based on scores that would be evident of the student mastering the material.

Dual-enrollment classes, on the other hand, function as a partnership between high schools and colleges. A dual-enrollment class holds high school students to the college-level standard and curriculum. The students then pay per credit at the partnered college’s rate and receive those credits upon class completion as if they were taking those courses on the college campus. Both types of classes can save students and parents valuable time and money in their pursuit of higher education.

- Familiarize yourself with the aid process

There are many types of student aid, and amounts can vary based on a plethora of factors. The most obvious form of assistance provided to students is scholarship money. It can be awarded based on test scores, academic results, athletics or extracurricular activities, and amounts can fluctuate based on a student’s choice of school. There are also opportunities for privately-funded scholarships that can be awarded by foundations, religious groups or other organizations on a need or merit-based basis. Students can typically find these opportunities online and apply if they meet predetermined criteria.

Students should also fill out the Free Application for Federal Student Aid, otherwise known as the FAFSA [5]. The FAFSA uses a student’s information to determine how much aid they might qualify for, including money from grants or state-funded assistance. It can also determine how much a student could qualify for in loans if those become necessary.

- Familiarize yourself with current legislation

Legislation is always changing for parents looking to get a jump-start in funding their child’s education. For example, the FAFSA Simplification Act of 2020 opened new doors for students trying to qualify for need-based assistance. Prior to the FAFSA Simplification Act of 2020, the FAFSA calculated the expected family contribution, or the EFC. The EFC estimated the amount family members would be able to contribute to a student’s education based on income, assets and other benefits. EFC has now been replaced by student aid index, or SAI. Where EFC bottomed out at $0, SAI can go as low as -$1,500, meaning students can qualify for more need-based aid [6]. SAI also simplifies the form itself, cutting down the number of questions and the factors that figure into assistance a student might receive from family.

Where this could truly be a boon to students who need more aid is through family members whose contributions were accounted for in the EFC but are not accounted for in the SAI. The popular 529 plan, which provides tax-advantaged savings for designated beneficiaries, is often used by grandparents to help their grandchildren pay for college. Funds from a 529 plan no longer factor into the expected contributions from family members meaning that they will not have negative implications for the FAFSA’s estimation of how much aid a student requires [7].

- Research schools prior to selection

Cost can differ by school selection, and though some students have their hearts set on a specific university, financials could play a large role in deciding on the best fit for your child. For example, students who do not expect to receive much aid from family or scholarship opportunities can opt for community college. Community colleges generally offer favorable per-credit prices for in-state students. The average cost per credit hour at a two-year community college is $141 while a public, four-year university costs $390 per credit hour on average [8].

After two years at a community college, students can usually transfer their credits to a university to finish a four-year degree. Wide-ranging opinions also exist about college selection [9]. Some researchers and surveys suggest that attending a prestigious college could be nothing more than a status symbol. Employers can look for many qualifications such as experience, extracurriculars, ability or the simple fact that a candidate attended any college. At the end of the day, the right choice of school will be different for each student.

If you have any questions about saving or planning to help your family, please give us a call! You can reach Bulwark Capital Management at 253.509.0395.

Trek 284

Sources:

- https://www.ellucian.com/assets/en/white-paper/credential-clout-survey.pdf

- https://www.forbes.com/sites/michaeltnietzel/2021/10/11/new-study-college-degree-carries-big-earnings-premium-but-other-factors-matter-too/?sh=6fd5ad4035cd

- https://www.usnews.com/education/best-colleges/paying-for-college/articles/2017-09-20/see-20-years-of-tuition-growth-at-national-universities

- https://apcentral.collegeboard.org/exam-administration-ordering-scores/ordering-fees/ordering-exam-materials/help/cost-of-exam

- https://studentaid.gov/

- https://unicreds.com/blog/student-aid-index

- https://www.usnews.com/education/best-colleges/paying-for-college/articles/tips-for-grandparents-using-a-529-plan-to-save-for-college

- https://educationdata.org/cost-of-a-college-class-or-credit-hour

- https://www.nbcnews.com/business/business-news/does-it-even-matter-where-you-go-college-here-s-n982851

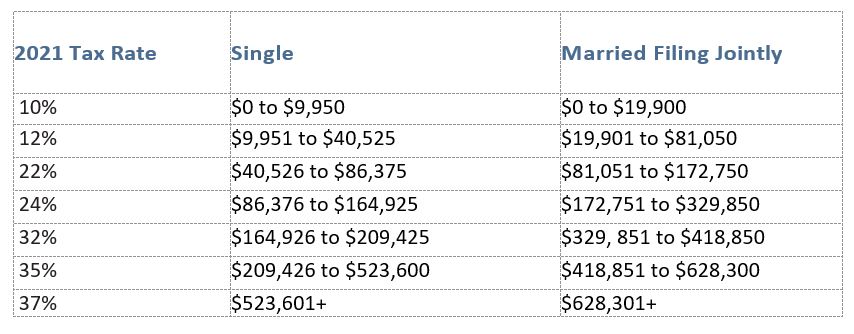

NOTE: These tax rates are scheduled to expire in 2025 unless Congress acts to make them permanent [9].

NOTE: These tax rates are scheduled to expire in 2025 unless Congress acts to make them permanent [9].

253.799.6416

253.799.6416 invest@bulwarkcapitalmgmt.com

invest@bulwarkcapitalmgmt.com