Although many of us are still recovering from the hustle and bustle of the holidays, tax season is just around the corner. Getting organized early puts you in a stronger position to avoid penalties, interest, and last-minute stress before the April 15 deadline. As you prepare to file your 2025 tax return, it’s important to keep upcoming tax changes in mind and to be aware of remaining contribution opportunities before key deadlines.

Standard deduction

For tax year 2025 (returns filed in 2026), the One Big Beautiful Bill Act (OBBBA) raised the standard deduction amount to $31,500 for married couples filing jointly. For single taxpayers and married individuals filing separately, the standard deduction for 2025 is $15,750, and for heads of households, the standard deduction is $23,625. For 2026, the standard deduction amounts are even higher: $32,200, $16,100 and $24,150 respectively.

Retirement contributions

There is still time to make contributions that count toward the 2025 tax year. It is important to make or adjust contributions before these deadlines.

- Individual retirement accounts (IRA/Roth IRA): For tax year 2025, individuals may contribute up to $7,000 to an IRA or Roth IRA. Individuals age 50 and older may make an additional $1,000 catch-up contribution. Contributions for 2025 can generally be made up until the tax filing deadline of April 15, 2026.

For 2026, the annual contribution limit increases to $7,500 for those under 50, and $8,600 for those 50 and older.

- Employer-sponsored retirement accounts: For 2026, the annual employee contribution limit for 401(k), 403(b), governmental 457 plans, and the federal government’s Thrift Savings Plan increases to $24,500 (up from $23,500 for 2025).

Individuals age 50 and older may make an additional $8,000 catch-up contribution, allowing total annual contributions of up to $32,500. Individuals ages 60 through 63 may be eligible for a higher catch-up contribution limit, subject to plan provisions.

Health savings accounts (HSAs)

- For tax year 2025, HSA contribution limits are $4,300 for self-only coverage and $8,550 for family coverage.

- For 2026, the limits increase to $4,400 and $8,750, respectively. Individuals age 55 and older who are not enrolled in Medicare may contribute an additional $1,000 catch-up amount in either year.

Planning starts now

Other notable changes and phase-out limitations for 2026 include adjusted tax brackets for ordinary income and capital gains, increased contribution limits for retirement accounts, and updated thresholds for certain credits and deductions, including dependent- and education‑related benefits, and more. A list of these adjustments for tax year 2026 is available on the IRS website.

By staying informed about 2026 tax changes and taking advantage of remaining 2025 contribution opportunities, you may feel more confident approaching the upcoming tax season. If your tax situation is complex, consider consulting a tax professional for guidance. Most audits happen because of simple mistakes, like missing forms, mismatched income, wrong Social Security numbers, or filing before you have everything you need. Coordinating financial and retirement planning with trusted tax professionals can support alignment and reduce the likelihood of common filing errors.

Make tax season less stressful. Contact us today to review your financial and retirement plan and discuss personalized strategies.

This article is for general information purposes only from sources believed to be accurate. It should not be construed as tax advice. In every case, you should consult with your own personal team of tax, financial, and legal advisors for tax advice specific to your own personal financial situation.

Sources:

- https://www.irs.gov/individuals/get-ready-to-file-your-taxes

- https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

- https://www.irs.gov/newsroom/what-taxpayers-can-do-to-get-ready-for-the-2026-tax-filing-season

- https://www.fidelity.com/learning-center/smart-money/hsa-contribution-limits

- https://www.fidelity.com/learning-center/smart-money/roth-ira-contribution-limits

- https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

Disclosure:

Investment Advisory Services offered through Trek Financial LLC, an investment adviser registered with the Securities Exchange Commission. Information presented is for educational purposes only. It should not be considered specific investment advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the sale or purchase of any securities or investment strategies. Investments involve risk and are not guaranteed, and past performance is no guarantee of future results. For specific tax advice on any strategy, consult with a qualified tax professional before implementing any strategy discussed herein. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. Trek 26-20

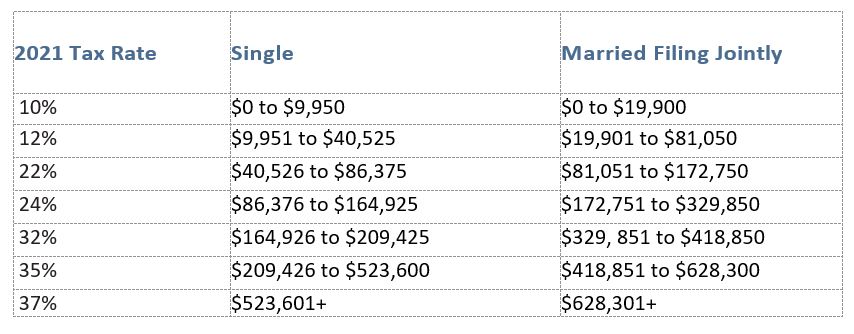

NOTE: These tax rates are scheduled to expire in 2025 unless Congress acts to make them permanent [9].

NOTE: These tax rates are scheduled to expire in 2025 unless Congress acts to make them permanent [9].

253.799.6416

253.799.6416 invest@bulwarkcapitalmgmt.com

invest@bulwarkcapitalmgmt.com