National Annuity Awareness Month is upon us! Let’s go over how annuities can be an important part of a retirement plan.

June is National Annuity Awareness Month, giving us the perfect reason to discuss how they can positively impact your retirement. Annuities have always played a role in retirement planning, but with growing uncertainty and market volatility, their importance has boomed. They offer the chance for growth along with the protection of principal during market downturns which is guaranteed by the claims-paying ability of the issuing insurance carrier.

While they can be a vital part of the retirement-planning process, annuities can sometimes be overlooked by advisors who focus strictly on accumulation and stock market investments. For people getting close to retirement and those without the appetite or flexibility for stock market risk, annuities can be an attractive option to guarantee income for life.

In fact, annuities were created for retirement; they were first invented during ancient Roman times to compensate retired soldiers. They’re meant to help you generate income once you stop collecting wages. There are many different types of annuities, but fixed and fixed indexed annuities are different than retirement accounts like 401(k)s and IRAs in that they are not subject to market risk, and they offer guarantees.

In other words, fixed and fixed indexed annuities can offer a guaranteed income stream to eliminate some of the uncertainty that comes with retiring. It’s important to understand fixed and fixed indexed annuities are not investments, they are contracts. Even though they may credit interest based on market gains, they are not actually invested in the market at all. Fixed and fixed indexed annuities are contracts between you and the issuing insurance company, who again, based on their claims-paying ability, guarantee your principal and sometimes offer participation in stock market upside.

One of the main concerns of Americans on their way into their golden years is funding a secure retirement. In fact, a recent study showed that 56% were worried about running out of money in the next stage of their lives [1]. That worry seems to be well-founded, as a 2019 study projected that over 40% of U.S. households will run out of money in retirement [2].

One of the biggest reasons retirees run out of money is sequence of returns risk. This can happen when clients withdraw money from accounts early in retirement in a down market. The withdrawals can then out-pace the growth of the account, making it more likely that a person completely drains their funds while still living.

A fixed indexed annuity can counter sequence of returns risk by providing a guaranteed lifetime income option. Under a properly-structured fixed indexed annuity, the principal and the lifetime income benefit are both protected, which can be beneficial in a market crash. They also offer flexibility in diversifying your portfolio, as retirees with a guaranteed lifetime income benefit can keep other assets invested in the market, conceivably giving them a chance to wait out valleys and plateaus.

Some annuities are even designed to help combat inflation by offering a COLA, or cost of living adjustment. Considering the 2021 inflation rate was the highest America has seen since 1981[3], it’s no wonder experts are expecting an increase in inflation-protected annuities [4].

While annuities are popular among those looking for protection as well as growth potential, purchasing one can be treacherous without proper help. There are many different types of annuities, and they won’t all offer identical benefits or protections. For example, variable annuities are directly invested in the market and carry the same risk that any market investment would. There are pros and cons to each type, and innovative insurance companies are working to design new annuity products with enhanced benefits every single day.

If you have any questions about annuities or how to protect your retirement funds, please give us a call! You can reach Bulwark Capital Management at 253.509.0395.

Sources:

- https://www.nirsonline.org/wp-content/uploads/2021/02/FINAL-Retirement-Insecurity-2021-.pdf

- https://www.ebri.org/content/retirement-savings-shortfalls-evidence-from-ebri-s-2019-retirement-security-projection-model

- https://www.thebalance.com/u-s-inflation-rate-history-by-year-and-forecast-3306093

- https://ifamagazine.com/article/inflation-could-lead-to-a-resurgence-in-popularity-of-annuities-says-continuum/

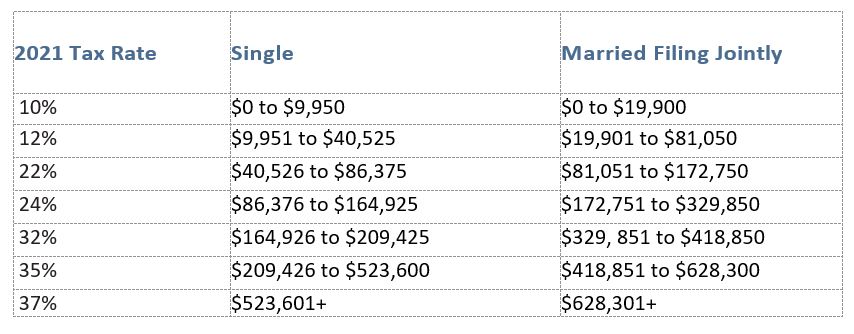

NOTE: These tax rates are scheduled to expire in 2025 unless Congress acts to make them permanent [9].

NOTE: These tax rates are scheduled to expire in 2025 unless Congress acts to make them permanent [9].

253.799.6416

253.799.6416 invest@bulwarkcapitalmgmt.com

invest@bulwarkcapitalmgmt.com